A 2023 report by security.org found that 58% of Americans fall victim to fraudulent credit card charges at some point in their lives. And when that happens, they contact their banks and credit providers for refunds – and if you’re a merchant, that’s coming out of your pocket.

Fair play? Not always. It’s not justå cases of genuine fraud that lead to chargebacks: Justt’s 2023 Chargeback Pulse research has found that 55% of customer disputes departments regard so-called “friendly fraud” (aka first-party misuse) as an evolving challenge. These are cases where consumers request a chargeback after receiving purchased goods or services, without a valid reason for dispute. Friendly fraud can occur for various reasons including mistaken purchases or customers forgetting a purchase, as well as a customer trying to ‘game the system’; either way, these chargebacks can still be costly and time-consuming for merchants to dispute.

But there are steps you can take to reduce the likelihood of becoming a victim of chargeback fraud. In this guide, we’re going to explore what chargebacks and friendly fraud are, how they work, and how you as a merchant can prevent chargebacks and implement safeguards against them.

Let’s start with the basics…

What are chargebacks?

Chargebacks occur when a cardholder disputes a transaction on their account and requests that their bank or card issuer reverse the charge, thereby removing funds from the merchant of record (the payee’s) account and recrediting the cardholder's account.

Chargebacks serve an important and legitimate role in finance: they protect consumers from a wide range of problems that can arise when purchasing products or services (e.g. defective goods), or just by having a credit card (e.g., identity theft and unauthorized transactions).

Some of the more common reasons for chargebacks include:

- Fraudulent transactions: Charges made without the cardholder's authorization.

- Billing errors: Incorrect amounts or duplicate charges.

- Non-receipt of goods: Goods or services were not delivered or provided.

- Merchant errors: Problems with the order processing or customer service.

- Defective products: Products that were not as described or were defective.

Chargebacks are most commonly associated with credit card transactions, but debit card chargebacks can and do happen depending on the bank and jurisdiction, as well as chargebacks on Paypal.

How do chargebacks work? How are they different from refunds?

Chargebacks are often misunderstood by merchants and confused with refunds, but they are entirely different.

While merchants can decide whether to give a customer a refund, they have no say over the chargeback process; disputed funds are forcefully removed from their bank account because the chargeback process reverses the disputed transaction. As a result, merchants must be fully aware of what they are and how they work.

Below portrays a general flow for a chargeback. However, the chargeback stages, timelines, and rules can be quite different across the different card schemes, so it is very important to understand the nuances of each chargeback type for each card scheme:

- Cardholder initiates chargeback: The cardholder disagrees with or identifies a problem transaction on their account. They contact their card issuer to dispute the charge and provide details about what’s wrong.

- Card issuer investigates: The card issuer will investigate the dispute by reviewing the claim and gathering evidence from the cardholder. The issuer then submits the chargeback into the card scheme network, and the chargeback flows to the acquirer, PSP, and ultimately to the merchant who loses the funds plus additional chargeback fees.

- Merchant responds (Representment): The merchant’s bank (acquirer/PSP) will notify the merchant of the chargeback. The merchant will then have an opportunity to respond with evidence to show that the transaction is legitimate—e.g., receipts, proof of delivery, customer correspondence.

- Issuer decision made: The cardholder’s card issuer reviews the evidence supplied by the merchant and makes an initial decision:

- Merchant decision made (Pre-Arbitration): If the issuer rules in favour of the merchant then the case is closed, and the merchant recovers the chargeback funds. If the issuer does not rule in favour of the merchant, then the case goes to what is usually called the Pre-Arbitration stage, and the merchant needs to decide if they want to risk continuing the dispute.

- Card scheme decision made (Arbitration)- If the merchant decides to continue disputing the case, then it is up to the card scheme to make the final ruling on the case. Whoever loses at the Arbitration stage, loses the chargeback amount plus an additional fee that can be over $500.

Types of chargebacks

Chargebacks can be categorized depending on the reason for the dispute. Regardless of the type of chargeback, the cardholder’s goal is the same: to get their money back. Some of the main chargeback categories include (but are not limited to):

- Fraud-related chargebacks occur when a cardholder claims that a transaction was unauthorized or fraudulent, such as:

- Fraudulent use of card information online, which is called card not present fraud

- The cardholder did not authorize an in store transaction, which is call card present fraud

- Processing error chargebacks occur when a merchant makes a mistake or some other oversight that causes:

- The same transaction to be processed more than once, which is called duplicate processing

- An amount being charged otherwise than that agreed to.

- Consumer dispute chargebacks occur when a cardholder is dissatisfied with the product or service purchased, such as:

- The merchant didn’t provide goods or services.

- The product or service might not be as described.

- Subscription charges continued after the cardholder canceled.

- The cardholder was promised a refund or credit that was not provided.

- Friendly fraud chargebacks/first-party misuse chargebacks: These can occur across all chargeback reason codes, and can range from innocent mistakes to deliberate fraud:

- The cardholder falsely claims that a transaction was unauthorized.

- The cardholder says that they did not receive their goods.

- The cardholder claims the product arrived damaged or broken.

- The cardholder claims they returned the goods but didn’t.

What is friendly fraud/first-party misuse?

We briefly mentioned this earlier. Friendly fraud (AKA first-party misuse), also known as chargeback fraud, occurs when a consumer makes a purchase using their credit card and then requests a chargeback from the issuing bank after receiving their purchase, without a valid reason for the dispute. It’s called “friendly fraud” because it’s perpetrated by otherwise unassuming, legitimate customers.

Friendly fraud can occur for various reasons, such as when a cardholder doesn't recognize a transaction on their statement, a family member makes a purchase without the cardholder's knowledge, or the cardholder simply forgets about a purchase they made. While some customers may deliberately attempt to receive something for free, many instances of friendly fraud are unintentional and stem from innocent mistakes or misunderstandings.

Friendly fraud is a rapidly growing pain point for merchants both big and small. Estimates say that it accounts for as much as 70% of all credit card fraud and costs the industry more than $132 billion a year. This cost doesn’t account for additional costs incurred by merchants, such as the loss of goods.

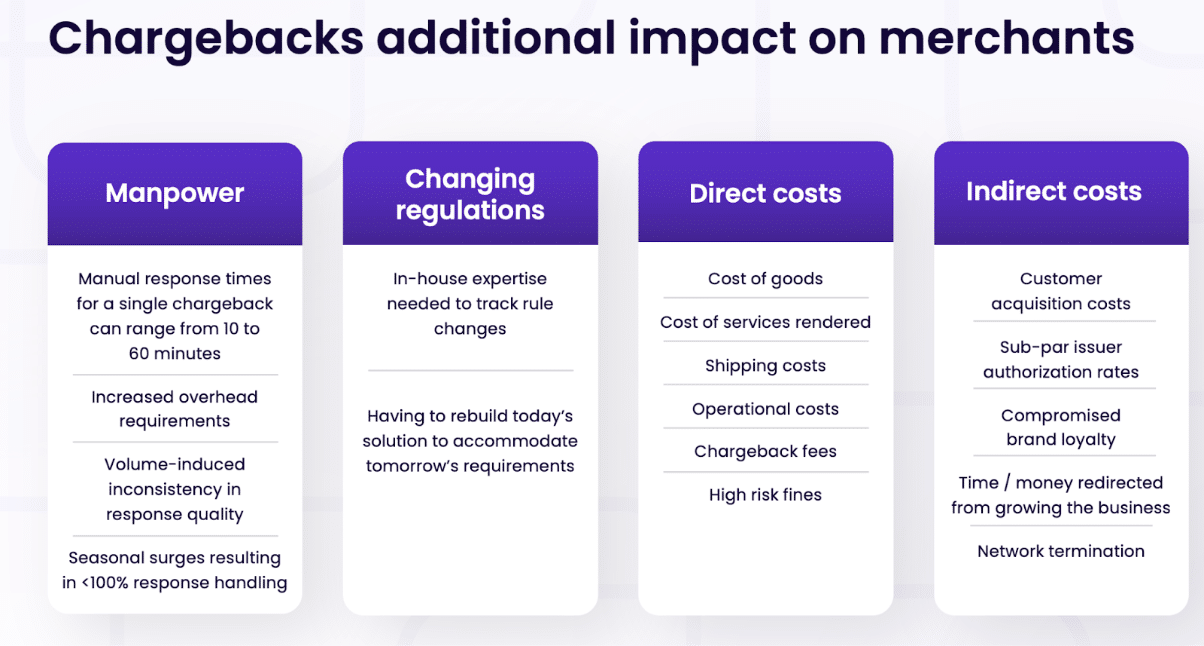

The cost and impact of chargebacks for merchants

Chargebacks can be extremely damaging for merchants, as they not only lose the product and the associated revenues of that sale, but they can also incur fees, penalties, and fines from payment processors and card networks. This is because merchants are usually charged a fee for each chargeback by their acquiring bank. These fees can vary but can add up quickly if multiple chargebacks are received.

The different card schemes charge different fees on chargebacks. However, since merchants receive most of these fees from their acquirers/PSPs, and not directly from the card schemes, they do not usually see the exact fees that the card schemes charge the acquirer, but rather the fees that the acquirer/PSP choses to charge the merchant on top of what the PSP is are charged by the card schemes. Many times the chargeback fee charged to the merchant is a higher fee than what the acquirer is originally charged by the card schemes. As a merchant it is important to understand what your PSPs fees are around chargebacks, and to see if you can negotiate any of these fees.

In addition to costs associated with chargeback fees and lost inventory, there’s a whole host of additional potential costs that also eat into merchants’ bottom lines:

- Administrative costs: When a customer initiates a chargeback, merchants need to consider whether they should attempt to build and send evidence against the chargeback. This requires time and effort and can be very expensive.

- Logistical costs: Processing an order involves operational costs such as production, packaging, shipping, and logistics. All of these costs are lost and non-recoverable when a chargeback occurs.

- 5%-25% impact on a merchant’s net income: When a chargeback is lost the entire amount is lost, and not only the merchants margin. For merchants with low margins, this can lead to a loss of up to 25% of their net income.

Due to these variables, it’s difficult to determine a precise cost of chargebacks to merchants. What we’ve found through our research, however, is that the average chargeback costs a business 2.5x the amount of the transaction as a baseline—so a $200 dispute would cost around $500 in total.

It's not all about costs, though. Managing chargebacks can be a resource-intensive process. Merchants must gather evidence, respond to chargeback notices, and often engage in lengthy dispute resolution processes. High chargeback rates can also damage a merchant’s reputation with customers and, in some situations, strain relationships between merchants and acquiring banks and payment processors. Merchants with high chargeback ratios may face higher fees, stricter contract terms, or even termination of their merchant accounts.

How merchants can avoid chargebacks

Chargebacks are inevitable. Businesses that sell products or services to customers will eventually need to deal with both legitimate and fraudulent chargebacks. Our 2023 Consumer Attitudes Towards Chargebacks survey found that 78% of U.S. consumers surveyed had filed a chargeback in 2023. 50% filed between one and two, and 12% filed six or more. We also found that compared to 2022, the number of U.S. and UK consumers who filed at least one chargeback in 2023 drastically increased.

This highlights a troubling trend for merchants, who not only face the uphill battle of proving the legitimacy of their charges in the face of chargebacks but also stand to lose the most as a result. Merchants must therefore make it an operational imperative to reduce their risk exposure by implementing processes, tools, and best practices that prevent them from occurring in the first place and put you in a strong position to fight those that do crop up.

1. Have clear refund, return, and cancellation policies

One of the most effective ways to prevent chargebacks is to establish and communicate clear refund, return, and cancellation policies. Ensure these policies are easy to find on your website and clearly explained at the point of sale.

Your policies should include detailed instructions on how customers can return products, request refunds, or cancel orders. By setting the right expectations and making the process straightforward, you can reduce the likelihood of misunderstandings that lead to chargebacks.

2. Work with reliable delivery partners

Timely and accurate delivery of products is essential to avoid chargebacks related to non-receipt of goods. Partner with reputable delivery services that offer reliable tracking and proof of delivery. Not only does providing customers with tracking information help build trust, but proof of delivery and receipt by the customer can provide valuable ammunition for fighting chargebacks.

This is especially important in some jurisdictions such as the United Kingdom, for example, where goods that are sold online remain “at the trader’s risk” until they come into physical possession of the consumer.

3. Use a clear billing descriptor on customer statements

A clear and recognizable billing descriptor on customer credit card statements is crucial for preventing chargebacks due to unrecognized transactions. The last thing you need is for your customer to look at their account and flag your legitimate transaction because they can’t figure out that it’s you.

To that end, make sure that the descriptor includes your business name or some other information that will make it recognizable. Ambiguous descriptors often lead to confusion and disputes, so clarity can significantly reduce chargeback incidents.

4. Use robust customer authentication

Credit card fraud is on the rise, so it’s never been more important for merchants to implement customer authentication as part of the checkout process. These can significantly reduce the risk of fraud-related chargebacks because they add an additional layer of security between you and genuine fraudsters. This includes authentication tools such as Address Verification System (AVS), Card Verification Value (CVV), and 3D Secure (e.g., Verified by Visa, MasterCard Secure Code). 3D secure will even help prevent fraud level chargebacks from happening in the first place as the liability shift will cause the cardholder’s claim of fraud to be the responsibility of the issuer.

Fighting chargeback disputes

Even if you did everything right, you’re going to be dealing with chargebacks, and a large portion of them will be illegitimate.

If a merchant believes a chargeback is fraudulent or invalid, they have the right to dispute it through a process called representment. To do this successfully, the merchant must present compelling evidence to the issuing bank that the original transaction was legitimate and that the chargeback is not warranted.

The type of evidence required will depend on the reason for the chargeback. For example, if the customer claims they never received the goods, the merchant should provide proof of delivery, such as a signed receipt or tracking information showing the item was delivered to the correct address. If the chargeback is due to a claim that the product was not as described, the merchant may need to provide detailed product descriptions, photos, or other documentation to prove that the item matched what was advertised. Merchants must submit this evidence within the time frame specified by the card issuer, which is usually a matter of days or weeks.

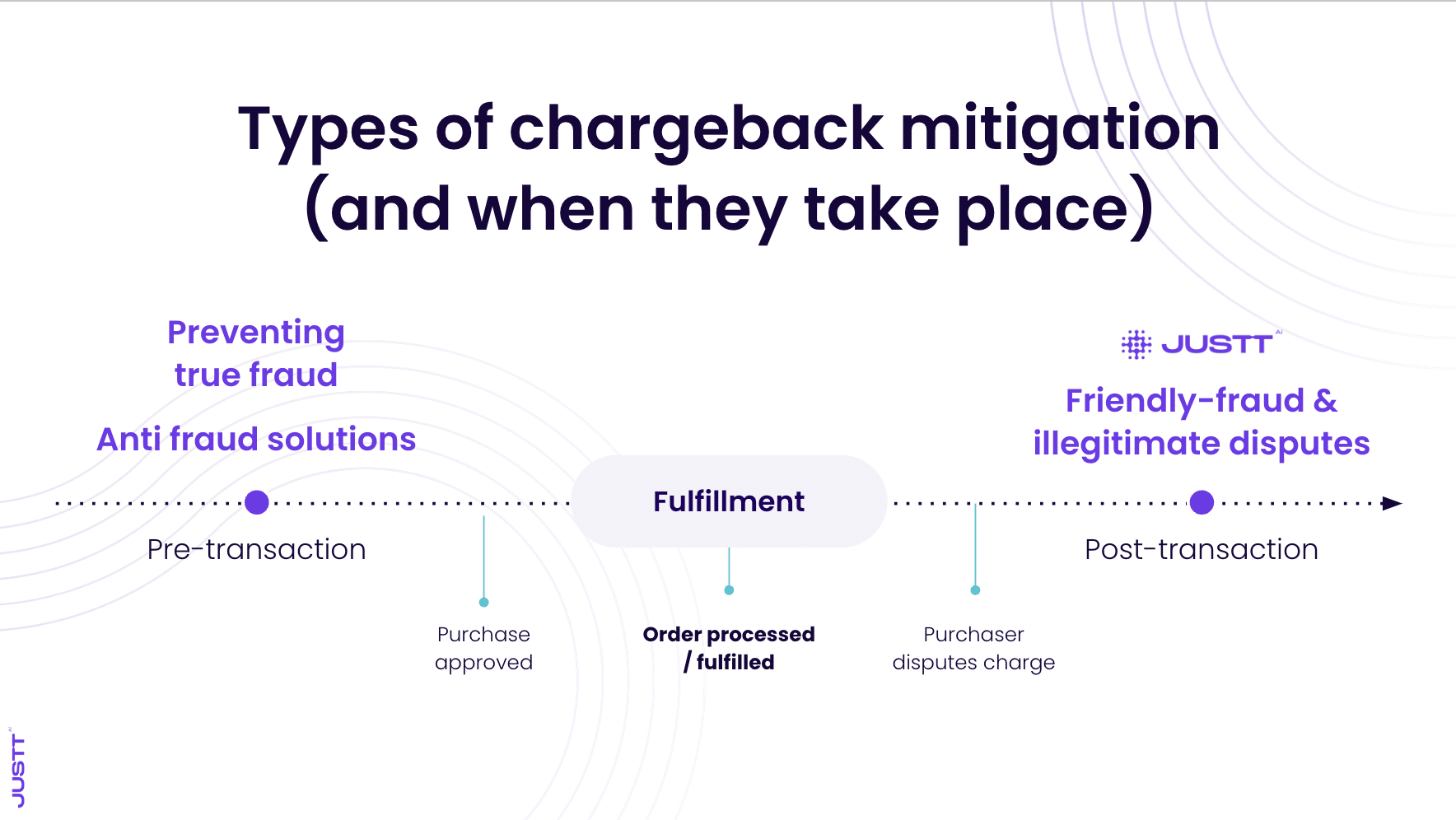

Types of chargeback mitigation tools

While many chargebacks are still disputed manually, and larger merchants might have dedicated departments dealing just with this issue, automation is quickly becoming the norm. In a world driven by technology, it’s increasingly clear that the only truly effective way to mitigate chargebacks is to deploy a comprehensive, data-driven defense strategy. Chargeback prevention and mitigation solutions work by helping both decrease the amount of chargebacks received and help recover the lost funds from chargebacks once they occur

The 2 main solutions can be explained as follows:

- Pre-transaction (prevention)- Anti fraud solutions are designed to identify true fraudulent transactions before they are approved in order to prevent fraud chargebacks from happening in the first place.

- Post-transaction (mitigation)- Chargeback mitigation solutions are designed to build evidence against friendly fraud/first-party misuse chargebacks in order to recover the lost funds from these chargebacks.

Different options exist in each category and they all take their own approach to managing chargebacks. It’s therefore important for merchants to research how a solution works, its features, and benefits, and whether these align with organizational needs.

On one end of the automation spectrum, Justt is completely hands-free and AI-driven. The platform will automatically build the merchant’s evidence per case with a tailored response using 3 main data sources: PSP data, 3rd party data enrichment, and merchant data. Instead of using templates, the system is built off of dynamic arguments which the system chooses and designs per chargeback based on the scenario and data available for the case. Then once several closed months are completed the system continuously optimizes dispute responses based on win rate analysis. There is no need for a payments department to be involved in a specific dispute.

Other automation solutions will provide a more partial solution - offering templates, analytics, or even outsourced teams to handle chargebacks. So it’s important to look past the marketing copy on the vendor’s website and understand which parts of the process the system will automate, and which will stay under the merchant’s responsibility.

Common merchant chargeback FAQs

What’s the difference between a friendly fraud/first-party misuse chargeback vs. a legitimate chargeback?

The key difference between friendly fraud and legitimate chargebacks is that friendly fraud is a type of chargeback. It occurs when a cardholder intentionally or unintentionally disputes a legitimate transaction without a valid reason.

A chargeback can be categorized as a friendly fraud chargeback when:

- The transaction is legitimate and authorized by the cardholder.

- The cardholder knowingly files a false claim.

- The intent is to obtain a refund while retaining the product or service.

Cardholders might wish to do this for various reasons. They could have buyer’s remorse, for example, or have allowed a family member to make a purchase on their card and then regretted their decision later. They may also simply want to try and get a product or service for free and, in some cases, may have simply forgotten they made the purchase or not recognize the transaction.

What are the most common reasons for chargebacks?

Chargebacks are an important financial tool and provide customers with recourse against merchants who fail to hold up their end of the bargain. Some of the most common reasons for chargebacks include:

- Fraudulent or unauthorized transactions

- Billing errors or duplicate charges

- Non-receipt of goods or services

- Goods or services not as described

- Technical errors during transaction processing

- Customer dissatisfaction or misunderstanding

What happens when a chargeback is filed?

Filing a chargeback kickstarts a structured dispute process. This process has different nuances per card scheme, but a general chargeback flow is as follows:

- The cardholder contacts their issuing bank to dispute the transaction.

- The issuing bank issues a provisional credit to the cardholder and investigates the claim, and submits a chargeback to the card schemes if they see relevant

- The merchant's acquiring bank is notified and requests evidence from the merchant.

- The merchant submits evidence to support the legitimacy of the transaction.

- The issuing bank reviews the evidence and decides to uphold or reverse the chargeback.

- If the issuing bank upholds the chargeback, the merchant has the ability to push the case to Arbitration.

- At Arbitration the card scheme will rule on the case and charge the losing party both the chargeback amount and an additional fee that can be over $500.

How long do customers have to file a chargeback?

The time frame for filing a chargeback varies by card scheme and industry type, but is typically 120 days from the transaction date. Merchants need to be aware of these time frames to manage disputes effectively.

Why are chargebacks allowed?

Chargebacks are a necessary component of the payment processing ecosystem. They serve as a protective mechanism for consumers against unscrupulous merchants and mistakes, help maintain trust in the financial systems, and encourage merchants to maintain high standards of service and security.

Are chargebacks free?

Chargebacks do not cost the consumer anything. In contrast, merchants are charged a chargeback fee. Merchants with a high chargeback to transaction ratio are more likely to be charged additional fees.

Automate your chargeback mitigation to win 2x more disputes

Justt is a hands-free chargeback mitigation tool powered by proprietary AI. It leverages over 500+ data points including customer attributes, geolocation, and device information to dynamically build credible cases against fraudulent chargeback claims (friendly fraud/first-party misuse chargebacks) and close disputes in your favour — all without you having to do any of the heavy lifting.

To see how Justt works in practice, sign up for a free product demo.