As payment networks continue to evolve their fee structures, Visa’s latest round of changes set to take effect April 1, 2025, signals a strategic shift toward incentivizing faster dispute resolution and more efficient processing protocols. These adjustments introduce tiered fee models for dispute management that can impact merchants across various sectors. While these fees target acquirers, not merchants, your PSP may pass them on to you. We recommend contacting your PSP to confirm. Understanding these changes is critical for businesses looking to optimize their payment operations and maintain healthy margins in an increasingly complex payments ecosystem.

Visa’s Interchange Updates & Fee Adjustments

As of April 1, 2025, Visa is adjusting its fees and dispute policies, introducing both cost increases and processing benefits for merchants. These updates emphasize higher fees for processing inefficiencies while rewarding businesses that align with Visa’s preferred transaction methods.

Changes in U.S. Dispute-Related Fees

Visa is introducing a tiered fee model for dispute responses, whether it be accepting or representing a chargeback, making chargeback management more expensive for merchants who take longer to act in either scenario. In this article, we’ll explain the difference in Visa’s fees and timelines for both accepting and responding to chargebacks.

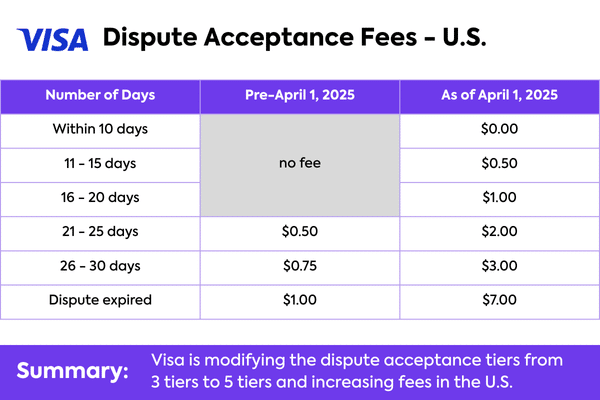

Changes in U.S. Acceptance-Related Fees

Below are the main changes that will be in effect on April 1, 2025 regarding acceptance fees in the U.S.

- Acceptance submitted within 10 days remains free.

- Acceptance submitted between 11–15 days incur a $0.50 fee per case.

- Acceptance submitted between 16–20 days incur a $1.00 fee per case.

- Acceptance submitted between 21–25 days incur a $2.00 fee per case.

- Acceptance submitted between 26–30 days incur a $3.00 fee per case.

Additionally, the dispute expired fee at the acceptance stage has risen to $7.00.

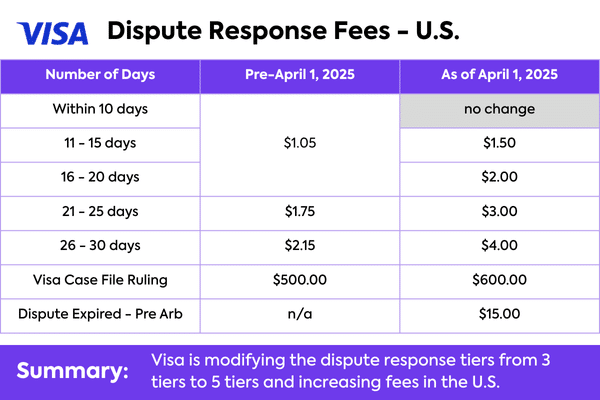

Changes in U.S. Response-Related Fees

There are also changes being made to the dispute response tiers as follows:

- Responses submitted within 10 days remain $1.05.

- Responses submitted between 11–15 days incur a $1.50 fee per case.

- Responses submitted between 16–20 days incur a $2.00 fee per case.

- Responses submitted between 21–25 days incur a $3.00 fee per case.

- Responses submitted between 26–30 days incur a $4.00 fee per case.

Additionally, the case file ruling fee is rising from $500.00 to $600.00. For merchants whose chargeback disputes go to arbitration, and lose, they will bear the cost of this fee, in addition to the chargeback funds that will be lost.

Furthermore, a new $15.00 “dispute expired” pre-arbitration fee is being introduced, emphasizing the importance of accepting a dispute even at the pre-arbitration stage, to avoid a $15.00 fee. We advise that merchants check with their PSPs to determine if they will handle this on the merchants behalf, or if the merchant is responsible for auto-accepting pre-arbs.

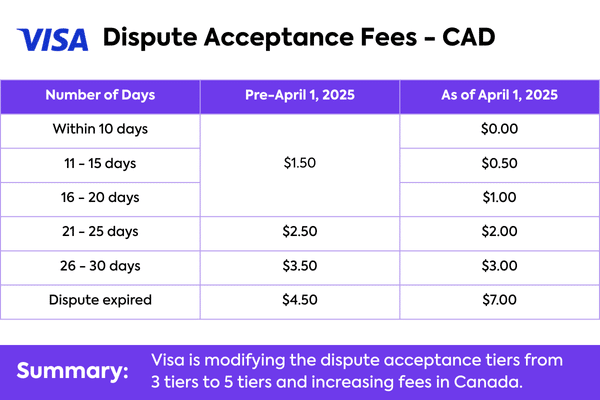

Changes in Canadian Dispute-Related Fees

For merchants operating in Canada, Visa is also modifying dispute-related fees, shifting the costs for both acceptance and responses on chargeback disputes. Businesses processing commercial cards, especially in recurring billing and emerging industries, should review cost projections for 2025 to account for these changes.

Changes in Canadian Acceptance-Related Fees

Below are the main changes that will be in effect on April 1, 2025 regarding acceptance fees in Canada.

- Acceptance submitted within 10 days is now free.

- Acceptance submitted between 11–15 days incur a $0.50 fee per case.

- Acceptance submitted between 16–20 days incur a $1.00 fee per case.

- Acceptance submitted between 21–25 days incur a $2.00 fee per case.

- Acceptance submitted between 26–30 days incur a $3.00 fee per case.

Additionally, the dispute expired fee at the acceptance stage has risen to $7.00, from $4.50.

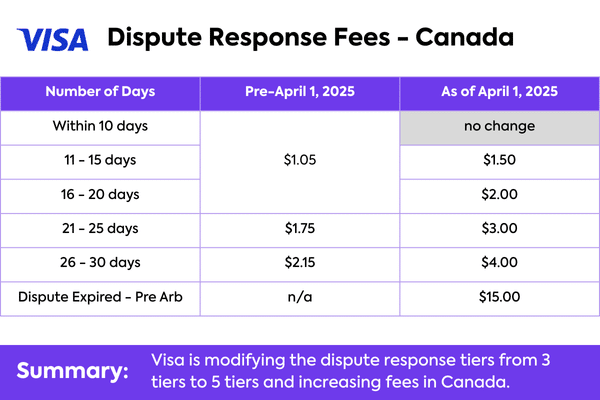

Changes in Canadian Response-Related Fees

Similar to the U.S.-based program, Visa is implementing a new structure to their response fees for Canada as of April 1, 2025.

- Responses submitted within 10 days remain $1.05.

- Responses submitted between 11–15 days incur a $1.50 fee per case.

- Responses submitted between 16–20 days incur a $2.00 fee per case.

- Responses submitted between 21–25 days incur a $3.00 fee per case.

- Responses submitted between 26–30 days incur a $4.00 fee per case.

Additionally, a new $15.00 dispute expired pre-arb fee at the response stage is being introduced.

Automatically Respond to Chargebacks with Justt to Minimize Response Fees

To avoid costly fees compiling, as well as missed chargeback cases, merchants can leverage AI-driven chargeback management tools like Justt. Justt seamlessly gathers and analyzes data from multiple data-sources to identify and present the best dispute response, while reducing response times to representing chargebacks.

In addition, Justt’s fully automated system provides consistent quality, even during periods of high volume. This comprehensive scalability is unlike other options on the market. Justt’s capability to fight chargebacks automatically, at any scale, can help save merchants from an insurmountable amount of late response fees over time. Click here to learn more about how Justt is revolutionizing automated chargeback management.

Accept Chargebacks with Justt to Avoid Higher Acceptance Fees

As seen previously, different levels of fees apply at different stages of the chargeback process. Some acquirers pass these fees onto merchants while others do not. Many merchants will want to accept certain chargebacks, under certain circumstances, as soon as possible to avoid compiling fees.

As mentioned, at Justt we proudly help merchants fight up to 100% of their chargebacks automatically. In the event a merchant prefers to accept a chargeback, we have features that empower merchants to take control and accept their chargebacks per PSP hassle-free, either manually or automatically with rule-setting logic. For example: a merchant can set a rule to accept all chargebacks that are less than $25.00.

We typically advise merchants to accept a chargeback if:

- A chargeback is correct and the cardholder should receive the money back

- Fighting a chargeback will cost the merchant more than the disputed amount, and the chances of winning are low

- The merchant does not have enough data to prove their claims

Given Visa’s fee changes, accepting and responding to chargebacks in a timely manner is more important than ever. Click here to learn more about our accept chargebacks feature.

Key Takeaways:

- Tiered Dispute Resolution Fees: Visa is implementing an updated time-based fee structure that rewards prompt action, with free processing for acceptance submitted within 10 days, but increased and escalating costs for delayed responses.

- Increased Arbitration Penalty Fees: Case file ruling fees have risen to $600, making processing inefficiencies significantly more expensive if a merchant loses a dispute in arbitration.

- Consistent Cross-Border Strategy: Similar fee structures have been implemented in both U.S. and Canadian markets, suggesting a unified approach to Visa’s global fee strategy.

Action Items for Merchants:

1. Ask Questions to Your Acquirer for Clarity: Understand your acquirer’s role in these changes, and how they are processing the updates.

Who is responsible for the fees?: Some acquirers will be passing these fees to their merchants. It’s important to understand who will bear the costs, and under what circumstances.

What are our timelines for responding to chargebacks?: Each acquirer processes chargebacks differently, and even if a merchant submits to the acquirer on time, with or without a solution provider, the acquirer still needs to get it to VROL afterwards. Given this, understanding how long it will take for them to process your disputes will be detrimental to avoiding or minimizing Visa’s fees.

Ask for clear communication: Merchants must have clear communication between their acquirers and solution providers to ensure, as chargebacks are processed, each party is clearly communicating and prioritizing each next step in the dispute process. Without clear communication, merchants could end up paying fees under circumstances that they are not liable for.

2. Audit Your Dispute Management Process: Review your current dispute resolution workflow to ensure responses can be submitted in a timely manner to avoid unnecessary fees.

3. Evaluate Automatic Chargeback Processing: Consider implementing a solution like Justt for AI-driven automatic chargeback management that responds quickly, compiling data from multiple sources to present the optimal dispute – saving merchants from paying costlier fees than necessary, and never missing a case. In addition, merchants can automate the acceptance of chargebacks, like low-value disputes where the cost of fighting exceeds the potential recovery amount and the chances of winning are low.

4. Review Processor Agreements: Determine whether your payment processor passes these fees directly to you or absorbs them, and factor this into your 2025 payment processing cost projections.

Visa’s April 2025 fee structure changes represent a clear pivot toward rewarding efficient transaction processing and timely dispute management. Forward-thinking merchants will view these adjustments not merely as cost increases, but as an opportunity to refine their payment operations. By optimizing workflows, implementing strategic acceptance rules for disputes, and responding promptly to legitimate chargebacks, businesses can minimize the impact of these changes while potentially improving their overall payment operations. As the payments landscape continues to evolve, the merchants who adapt quickest to these new parameters will gain a competitive advantage through lower processing costs and more streamlined operations.

Curious if these updates apply to your business? Speak with a Justt expert today to discuss >

Other Updates in the Ecosystem:

While Visa’s updates are significant for both U.S. and Canadian merchants, they are also modifying dispute fees for the Latin American & Caribbean (LAC) region, increasing fees for delayed responses beyond 21 days, and other fees. In addition, Mastercard and Discover are modifying their dispute fees for the U.S. region. Furthermore, Mastercard is also increasing their chargeback assessment fee for domestic disputes, and introducing a separate cross-border fee for cross-border disputes. Similarly, we recommend merchants contact their PSP(s) to better understand how these changes will impact them directly.