On April 1, 2026, Visa tightened its VAMP “Excessive Merchant” threshold from 2.2% down to 1.5% for merchants in the US, Canada, EU, and Asia-Pacific regions. It’s the kind of change that can trigger a reflexive scramble: new tools, new policies, new spend. But the right response depends entirely on where you actually stand.

This post explains what changed, who it affects, and how to think through your response, including when fighting chargebacks is still the smarter financial move.

Key takeaways at a glance

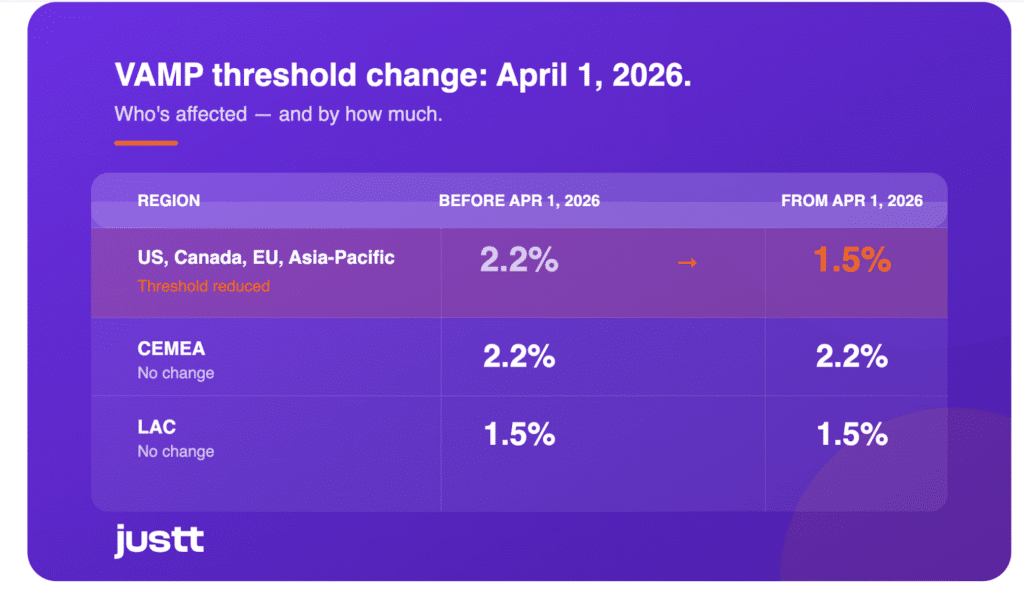

- Visa’s “Excessive Merchant” VAMP threshold dropped from 2.2% to 1.5% on April 1, 2026, but only for merchants in the US, Canada, EU, and Asia-Pacific regions

- The 1,500 combined fraud (TC40s) and dispute (TC15s) event monthly minimum still applies. Below that volume, you’re not formally in Visa’s sights

- Your acquirer’s internal thresholds may be stricter than Visa’s. That conversation is worth having now if you haven’t already

- Pre-chargeback alerts can reduce your VAMP ratio, but auto-refunding every Verifi alert isn’t always the right call

- If you’re comfortably within thresholds, many of those chargebacks are worth fighting

What is VAMP?

The Visa Acquirer Monitoring Program (VAMP) is Visa’s consolidated framework for monitoring fraud and disputes across the payments ecosystem. Launched in 2025, VAMP replaced five separate legacy programs, including the Visa Fraud Monitoring Program and the Visa Dispute Monitoring Program, streamlining them into a single global program with unified thresholds and a single remediation process.

The rationale is straightforward: the payments landscape has changed dramatically. The estimated cost of lost revenue to chargeback is currently $180 billion a year. It is one of the most under-reported costs in eCommerce. VAMP gives Visa a more coherent, globally consistent way to identify and address outlier risk.

Importantly, VAMP operates at two levels: it monitors both acquirer portfolios as a whole and individual merchants within those portfolios. Merchants who exceed their own thresholds can trigger scrutiny from their acquirer, which is why your PSP relationship matters so much in this context.

How is the VAMP ratio calculated?

The VAMP ratio is a single count-based metric applied to card-not-present (CNP) transactions:

VAMP Ratio = Count of [Fraud (TC40) + Disputes (TC15)] ÷ Count of Settled Transactions (TC05)

There are two things worth paying close attention to here:

- Fraud-related disputes are counted twice. A TC40 fraud report that subsequently becomes a TC15 dispute hits your VAMP ratio on both counts. This makes fraud-driven chargebacks disproportionately costly from a compliance perspective.

- There’s a minimum volume floor. In the AP, Canada, EU, and US regions, Visa only formally monitors merchants once they reach 1,500 combined TC40 and TC15 events per month. Below that threshold, you’re not in VAMP’s sights… BUT your acquirer may still apply their own standards.

The ratio also excludes TC15s (disputes) resolved through pre-dispute solutions like RDR and CDRN, and TC40 fraud reports that qualify under Compelling Evidence 3.0 on Order Insight, provided the timing of the data extract aligns. See Visa’s official VAMP fact sheet for full program detail.

What changed for VAMP thresholds in April 2026?

The headline change is a tightening of the “Excessive Merchant” threshold, i.e., the level at which Visa flags an individual merchant for elevated risk:

For merchants in the US, Canada, the EU, and Asia-Pacific (AP), that threshold dropped from 2.2% to 1.5% on April 1, 2026. In practical terms: a merchant who was comfortably within limits at a 1.8% ratio is now in excess of Visa’s threshold.

Who is NOT affected by this change?

Merchants in the CEMEA region (Central and Eastern Europe, Middle East, and Africa) remain at the 2.2% threshold

The 1.5% threshold already applied to merchants in LAC (Latin America and the Caribbean) since the introduction of VAMP. There is no change for these merchants.

Merchants processing fewer than 1,500 combined fraud reports and disputes per month are not formally monitored under VAMP in the AP, Canada, EU, and US regions. PLEASE NOTE: Your acquirer may still apply their own internal standards

Two tiers of VAMP identification

It’s also worth understanding that VAMP operates on two levels of severity, both of which apply at the acquirer portfolio level rather than directly to individual merchants:

- Above Standard: your acquirer’s overall portfolio ratio reaches 0.5% or above. Remediation is required.

- Excessive: the portfolio ratio reaches 0.7% or above, or an individual merchant within the portfolio exceeds the thresholds above. More serious intervention and potential fines apply.

In practice this means that even if your individual ratio is within Visa’s limits, your acquirer may come to you if their broader portfolio is under pressure. Another reason to keep that conversation open.

What Are the Consequences of Exceeding VAMP Thresholds?

The consequences depend on which tier you fall into.

At the Above Standard level, your acquirer must submit a remediation plan to Visa and will typically put pressure on the merchants within their portfolio who are contributing to the problem. Expect increased scrutiny and potentially tighter account terms.

At the Excessive level, Visa can impose fines directly on the acquirer, who may pass those costs downstream or terminate merchant accounts in serious cases. This is where consequences become material and fast-moving.

Beyond the financial impact, being identified as an Excessive merchant can affect your ability to negotiate favorable terms with payment partners and your broader standing within the acquiring ecosystem.

How to respond to changes in the VAMP threshold

Not every merchant needs to take action. The right response depends on your volume, your current ratio, and your acquirer’s own expectations. Here’s how to think it through.

Check whether you’re actually in scope

The 1,500 combined TC40+TC15 event floor still applies. If your monthly fraud and dispute counts fall below that, Visa isn’t formally monitoring you under VAMP. That doesn’t mean you’re free to be complacent because your acquirer may apply stricter internal thresholds. But it does mean the April 1st change may not be directly relevant to you right now.

One practical step that’s easy to overlook: make sure you actually have visibility into your own TC40 and TC15 data. To monitor your VAMP ratio you need access to both, and the experience varies significantly depending on your PSP. Some acquirers surface this data readily; others require you to request it explicitly, and it may take time to get. It is worth having that conversation now rather than after a problem emerges. In addition, Verifi offers TC40 data as a purchasable feed, which can be a useful supplementary source if your PSP is not forthcoming, though it may not capture every TC40 report filed against you.

Find out what your acquirer actually expects

Visa’s thresholds are the official standard, but many PSPs and acquirers maintain their own internal thresholds that are stricter than Visa’s. Your acquirer may flag merchants at 1.0% even though Visa’s “Excessive” line is now at 1.5%. The only way to know is to ask. Request a conversation with your acquirer about your current VAMP ratio, where they set their internal limits, and what the implications are for your account if you breach them.

Balance compliance with revenue recovery

Pre-chargeback alert solutions, which allow merchants to resolve disputes by issuing a refund before they become formal chargebacks, can help bring your VAMP ratio down. But if you’re comfortably within your threshold, automatically refunding every dispute through alerts may not be the smartest financial decision. Some of those chargebacks are worth fighting. Compliance is the floor, not the strategy.

Where pre-chargeback alerts fit in

Pre-chargeback alert services notify merchants of a potential impending dispute before it becomes a formal chargeback. Merchants can decide to issue a refund and prevent the chargeback from ever being filed. Because VAMP’s ratio formula excludes disputes resolved through pre-dispute solutions, using alerts effectively can reduce your VAMP exposure.

But alerts come with a cost. There is a direct fee per alert whether or not you issue the refund, and an indirect cost when a refund is issued on a dispute that could have been won. The right approach isn’t to resolve every alert automatically. It’s to understand your own situation:

- How close are you to your threshold? If you’re well within your VAMP ratio, you have headroom to be selective about which disputes you refund via alerts and which you contest.

- What does your acquirer expect? Some PSPs actively encourage alert resolution as a portfolio management tool. Others are more neutral. Know your acquirer’s position.

- What’s the win rate on your chargebacks? If you have strong evidence and either high win rates or a potential for high win rates on disputes, auto-refunding via alerts erodes revenue unnecessarily.

At Justt, we work with merchants on both sides of this equation, resolving disputes before they become chargebacks where it makes sense, and fighting chargebacks where the evidence supports it. The balance between the two looks different for every merchant, and it should be driven by your actual risk position, not by anxiety about a threshold change.

The bottom line

The April 2026 VAMP threshold change is real and worth understanding. For merchants in the US, Canada, EU, and AP regions who are running close to 1.5% and above the 1,500 TC40 and TC15 monthly count, it requires immediate attention. For merchants comfortably below that level, it’s an opportunity to review your setup, not a reason to overhaul it.

Compliance matters. But staying compliant and optimizing the revenue you recover from disputes aren’t competing goals. The merchants who come out ahead are the ones who understand their actual position and make deliberate decisions about which disputes to resolve, which to fight, and which tools to use to do both.

If you’re unsure where you stand or want to think through your chargeback strategy in the context of the new thresholds, talk to the team at Justt.