Note: In may 2025, Visa announced some significant changes to VAMP. Read this post for the latest information.

Visa has rolled out a new program that’s changing how merchants and acquirers are monitored for chargeback and fraud ratios. Keep reading to learn what you need to know.

The new Visa Acquirer Monitoring Program (VAMP) went into effect on April 1, 2025, consolidating the Visa Dispute Monitoring Program (VDMP) and Visa Fraud Monitoring Program (VFMP) within a unified framework. This consolidation aims to simplify and strengthen how fraud and chargeback activity is tracked across the payments ecosystem—for both acquirers and merchants.

Disclaimer: Visa is currently conducting internal evaluations and discussions to determine whether additional changes to the VAMP rules are necessary. More specifically, the key internal debate at Visa right now is whether their Verifi CDRN and RDR products will effectively cancel out TC40s from the VAMP ratios. Watch out for our next update as some of the details outlined below may evolve as the program develops.

For merchants, this means a new metric for monitoring chargebacks and fraud, and a shift in how tools for fraud prevention and dispute resolution impact your standing with Visa.

Key Aspects Of The New VAMP

Unified Monitoring System

By combining aspects of VDMP and VFMP, VAMP now provides a single dispute ratio to track.

VAMP Ratio Calculation

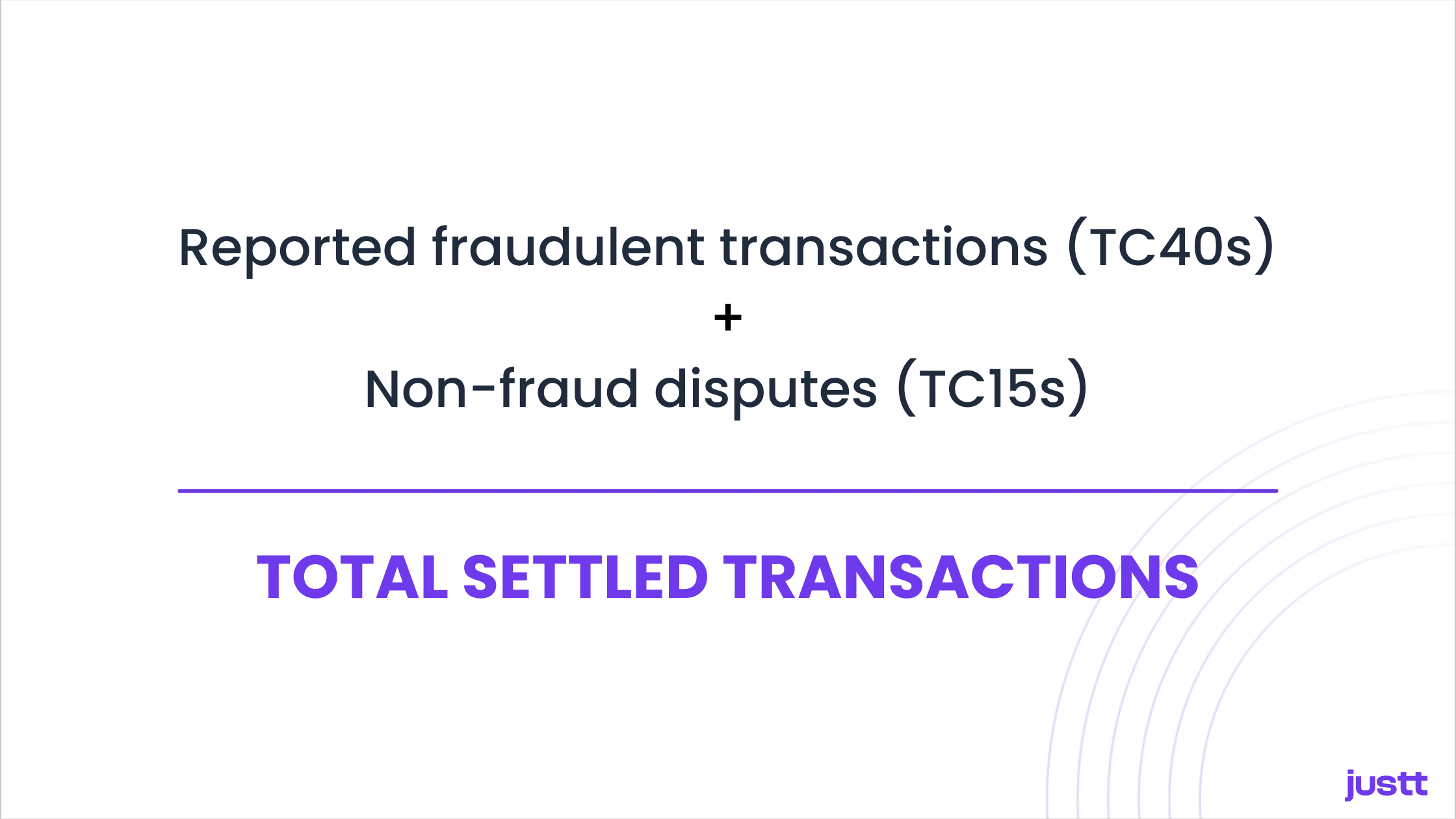

The VAMP ratio is determined by adding:

- Reported fraudulent transactions (sourced from TC40 data)

- Non-fraud disputes (including reason codes 11, 12, and 13, or TC15 messages)

Then, this total is divided by the number of settled transactions of that same month. Importantly, only card-not-present transactions are included in this calculation.

Note: Merchants who are used to calculating their VDMP ratios based on their volume of chargebacks should note that the new VAMP ratio is calculated based on TC40 and TC15 data, not total chargebacks. Importantly, when 3DS is used, the fraud chargeback is not posted against the merchant, but the TC40 is still filed on the fraudulent transactions. To accurately calculate their VAMP ratios, merchants who use 3DS must request their TC40 data directly from their PSPs.

Thresholds and Compliance

At launch, the thresholds are as follows:

- Merchants:

- “Excessive” VAMP ratio = 1.5%

- Drops to 0.9% starting January 1, 2026

- Acquirers:

- “Excessive” = 0.5%

- “Above Standard” = 0.3% (in effect from 2026)

Starting October 1, 2025, when the initial 6-month grace period ends, fines will be initiated if a merchant exceeds the limits for more than 1 month. However, merchants who are either new to the program or have maintained 12 consecutive clean months will receive an additional 3-month grace period. During this time, fines will not be applied. If the merchant achieves just one clean month within this 3-month window, they will automatically exit the program.

It’s also important to note that although Visa had initially planned for TC40 alerts to be excluded from VAMP calculations when a case was resolved through Verifi’s CDRN or RDR solutions, this functionality has recently been revoked. As of now, TC40s are still counted even if a resolution occurred via these tools. However, we are currently awaiting confirmation from Visa on whether this change is permanent or if the original exclusion rule will be reinstated.

Learn more about VAMP and how to stay compliant in our full Visa Acquirer Monitoring Program guide

Enumeration Ratio

VAMP also introduces a new way to track card testing fraud, known as the enumeration ratio. This measures how often fraudsters try to run small test transactions using stolen card numbers. The ratio is calculated by dividing the number of confirmed enumerated transactions by your total settled transactions.

Visa will use its new Account Attack Intelligence (VAAI) system to identify these attempts—technology that Visa says will reduce false alarms by 85%. If a merchant has fewer than 300,000 confirmed card testing attempts, they won’t be included in the program.

Advisory Period Extension for VAMP

Visa has extended the advisory period from three to six months, delaying enforcement until October 1, 2025. During this time, merchants who exceed thresholds will receive warnings but won’t face penalties—giving time to adjust before fees kick in.

Fees for Merchants: What’s at Stake?

Once the advisory period ends, merchants classified as “Excessive” will face fees of $10 per disputed or fraudulent transaction.

Even though acquirers are the ones who technically receive the fees from Visa, they’re highly likely to pass those costs on to merchants—and may even impose their own additional penalties or tighter thresholds to manage risk on their side.

What Merchants Should Do Now

The introduction of VAMP is a signal that Visa is raising the bar for fraud and dispute management. To stay compliant—and avoid fees—merchants should take action now:

- Make sure you have the data needed to monitor your VAMP ratio properly. If you are using 3DS, then you should have access to TC40s through your PSP so that you can properly calculate your VAMP ratios.

- Use Justt to represent your chargebacks, easily track your fraud and chargeback ratios of the different card schemes, and receive feedback when to use or not use alert solutions like Verifi and Ethoca.

- Strengthen fraud prevention with tools like anti-fraud solutions, 3D Secure, velocity checks, and device fingerprinting

- Collaborate closely with your acquirer to understand how they’re implementing VAMP and how it affects you.

- Stay up to date with new VAMP changes, as Visa is currently collaborating internally during this grace period to see if additional changes in the new VAMP rules should be changed.

The earlier you start, the better prepared you’ll be when the grace period ends in October.

Want help understanding how VAMP will affect your business—or how to get your chargeback ratio under control? Contact the experts at Justt today.